Crypto has made new millionaires all over the world. Since the explosion of Bitcoin, there has been enough time for everyone to hear about this new form of money. However, crypto has been the reason many people and companies went bankrupt last year when the market took a historic plunge. Blockchain technology that is the backbone of this ingenious invention has left most people confused, including those who have already invested in it.

What is the difference between blockchain and crypto? How do they two relate?

How did it evolve into something so great that it touches so many aspects of our lives?

Here is the simplest explanation:

Defining Blockchain and Crypto

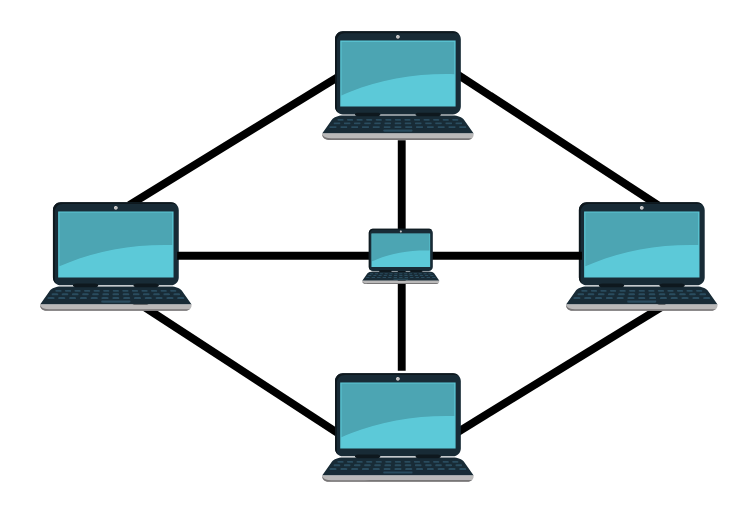

As the name implies, Blockchain is essentially blocks of encrypted information stored in a ledger, much like a spreadsheet, but on steroids. One block of data is linked to the previous, and that is how they form a chain. What makes this technology unique is the fact that it is a network of interconnected computers that don’t rely on one central entity to facilitate interaction. The connected machines make up the network itself, and they are based on a peer-to-peer system and on consensus.

The system relies on consensus among the peers in the network to make the changes in the train. In other words, entries become information, and a community of users control how the record is amended and updated. This is the backbone of each transaction on the technology.

Each peer is a computer system on the network and is also commonly referred to as nodes. Because the P2P network is continuously recorded and interchangeable between the nodes in the network, they differ from the traditional centralised client-server models. This method of transferring information is a massive improvement since the data isn’t kept at a single point, making the blockchain the ideal technology to protect the information stored in the blocks.

Think of it this way: the information on the blockchain is distributed but not copied.

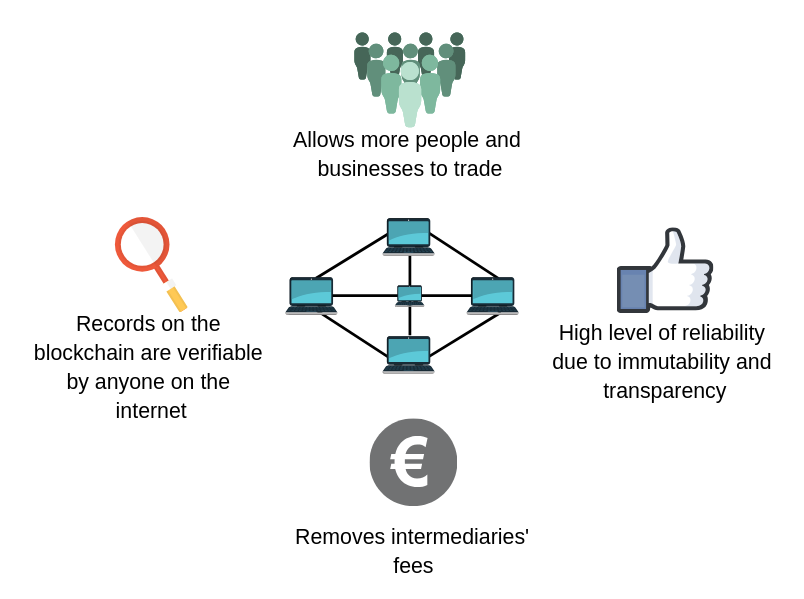

The interlinked blocks of information are immutable, much like a spreadsheet whose entries are connected but cannot be altered. This one property is what makes blockchain the ideal technology for recording and conducting transactions (of all kinds, from payments to insurance, to trade), in voting and virtually every industry today. Since all the parties in the network need to authenticate the chain of information, it is secure and ‘trusted’. This trust is what forms the basis of crypto.

Blockchain is

- Transparent and incorruptible

- Secure – Has no single point of failure

- Decentralized – Can’t be controlled by any single entity

So, what is crypto?

In computer science, cryptography refers to a communication and information security technique derived from the mathematical concept of using rule-based algorithms to encrypt a message in a way that makes it difficult to decipher.

When this mathematical concept is combined with the features of the blockchain, they create a platform on which units of events can be regulated, and ownership transfers can be verified independently of a third-party or a central authority such as a government. Blockchain technology created the backbone of the new internet. Cryptocurrency is the first application of blockchain.

Of the most known virtual currency, we have Bitcoin, which was invested by the still unknown, Satoshi Nakamoto. He announced Bitcoin in late 2008 as a “peer-to-peer electronic cash system”. He wanted to build a cash system without a central entity, like a file sharing P2P network, to avoid double spending.

“Every informed person needs to know about Bitcoin because it might be one of the world’s most important developments.” —Leon Luow, Nobel Peace Prize nominee.

The Bitcoin is the first and the most famous cryptocurrency of over 1500. It revolutionized digital currencies because of its most important, and most simple characteristic: it is a limited entries database that no one can change without fulfilling specific conditions. There’s a whole mechanism that backs the ruling of cryptocurrencies. To perform a transaction, it needs to be broadcasted in the network, sent from one peer to every other peer, until it is confirmed. Once it’s approved. It can’t be changed or deleted, it becomes part of an immutable (permanent) record, the blockchain.

By making it possible for encrypted information to be distributed but not copied, blockchain became the backbone of a new kind of internet that can keep its own money. All the digital currencies starting with Bitcoin, and the potential of smart contract platforms such as Ethereum are all made possible by the Blockchain technology.

Crypto, therefore, is one of the by-products of the blockchain.

Crypto’s regulatory issues

Cryptocurrency is a volatile currency. For this reason, it must be regulated to protect everyone who buys or uses it. The number of cryptocurrencies that went bust soon after public offerings are proof enough that more should have been done to regulate it. As governments around the world have been researching ways to deal with this new monetary system, the main concerns lie within protecting the economy, consumer protection and tax compliance. Here are some of the main regulatory issues that must be addressed.

Money laundering

The massive increase in the Bitcoin price in 2017 meant that the regulatory sector was scrambling to keep up. The legality of cryptocurrencies are yet to be decided in many jurisdictions, and the biggest concern is how they are being traded to break the law. As crypto gained popularity and started being accepted around the world, so too was the need to put in place regulations to prevent launderers. This is a serious issue that is subject to different rules in different territories, proving to be a challenge to enforce.

The decentralized and anonymous nature of many cryptos has raised many antennas among watchdogs, who fear that platforms are being used to launder money. Last year, the G20 member countries were keen on settling a global anti-money laundering standard for cryptocurrencies.

This concern goes hand in hand with the fear that cryptos are being used for other criminal activities online. A report, released last year, stated that the use of Bitcoin to fund illegal activities had dropped. Even though the number of transaction multiplied, the tracking and regulating of the currencies have resulted in less suspicious activities.

Securities and commodities regulations

In an attempt to overcome crypto’s instability, the crypto community is now turning to money-backed stable coins. This new product is specifically designed to be an asset-backed security and should be easier to regulate using existing laws.

The preference for a more secure form of investment comes after the rise and fall of Initial Coin Offerings (ICOs), which proved to be a very easy way to raise money, yet provided no security for investors as many of the projects didn’t go past the fundraising phase, and the tokens didn’t yield anything other than a headache. Security tokens have thus become 2019’s buzzword.

Differently from utility tokens, security tokens put a percentage of the ownership into the hands of the investor because they are a digitalised form of security. These digital assets rely on smart contracts, yet they behave like traditional securities and fall under the same set of regulations. They’ve become the preferred method to conduct a crowdfunding as they provide a secure framework for all the parties involved.

This means regulatory compliance procedures that change according to each country. The most well-known is the US Securities Exchange Commission (SEC), which have taken a skeptical stance towards crypto-assets and require an extensive list of documents for those that want to conduct a token offering.

Personal Privacy and Identity

Blockchain is a public ledger where each transaction is encoded and recorded in the public for anyone to look at. Of course, this doesn’t mean anyone can be able to identify the participants in a transaction, but still, anyone is justified in wondering how safe their information is on the public domain. Longstanding norms have made everyone concerned about where their personal, legal, financial, and even health data is stored.

In Europe, one of the largest concern when implementing the blockchain technology is the General Data Protection Regulation (GDPR). It is claimed that GDPR is incompatible with the blockchain because of the “right to be forgotten” clause. Effectively, once data has entered onto the blockchain, it cannot be deleted. However, the GDPR states that anyone within the EU can request that any personal data held about them can be permanently removed.

Finding a solution to create a GDPR compliant blockchain architecture has been a challenge, and yet again, depends on regulations. While there are some solutions proposed, such as off-chain storage, the protection of consumers’ private data can prove to be more beneficial by using blockchain and its guarantee of anonymity. However, it has become an issue for governments, as detailed in the previous section.

Some countries have imposed severe crackdowns on cryptocurrencies, such as China and Iran. However, others have chosen to regulate it as a way of attracting investors and protecting consumer and investors rights. In Europe, several nations have proven to be blockchain and crypto-friendly, attracting not only companies willing to conduct regulatory compliant crowdfunding but also regulated crypto exchanges. In Asia, we’ve recently seen how the Philippines has established token offering regulations and how Thailand is becoming a blockchain hub.

Blockchain disrupting industries

Blockchain is in many ways a miraculous technology innovation that has quickly made its impact felt in almost every sector in modern day life. From finance technologies and agriculture to data security and healthcare, blockchain is now being leveraged to improve the performance and efficiency of any operations that are handled by computers. Blockchain has been most impactful in these industries:

Fintech

Businesses and individuals have found blockchain’s smart contracts invaluable in revolutionizing how goods and services are traded. These digital agreements are better than traditional paper agreements in many ways, but the most important is that it is distributed and verifiable. Smart contracts have improved trust in the financial sector and have constituted an on-going challenge to legacy systems.

Trading

The trading industry has been benefiting from blockchain. To ensure that transactions are safe, governments, import and export companies, producers, supermarkets and even consumers are excited to apply blockchain in the tracking of products. This means that the supply chain’s steps are being digitalized and stored on the blockchain. The industries affected are many and varied. Most recently, Ford Motor Company has partnered with IBM to use technology to trace ethically sourced cobalt. Similarly, but in a completely different industry, South Korea and the United Kingdom are using the technology to track beef from the field to the slaughterhouse, to the supermarket shelf.

Energy micro-grids

Energy is an industry that has been growing significantly with the use of blockchain. It enables neighbours to buy and sell renewable energy generated and stored on the microgrid. We’ve covered several initiatives in this field. For example, South Korea’s ‘Future Micro Grid’ is a framework that will create an open energy community. With the use of blockchain, electricity can be traded without any difficulty across multiple micro-grids. In Bangkok Thailand, neighbours are buying and selling energy between themselves via the city’s electricity grid using blockchain.

Identity management

As the world gets more digitized, there is a need to have a system in place that can be relied upon to manage people’s’ identity on the internet. The distributed ledger technology can make it possible for users to have a unique and trusted identity management system that will revolutionize how individuals and businesses connect and communicate online.

The issue of privacy seen above has a direct correlation with identity. Securing every person’s identity in the digital world is not an issue that technology alone will solve; our sense of belongingness goes deeper to include culture, legal, education, business, life processes and our technological frameworks. Blockchain technology is already making significant progress to necessitate regulation of all these elements of identity in various industries.

Blockchain systems are being designed to respect the privacy of data and transactions on its platform. This application of blockchain is being used in several sectors, from conducting Know Your Customer (KYC) processes, to a blockchain-based digital identity system for payments, to self-sovereign IDs to help refugees rebuild their lives.

Intellectual property rights

It is easy to reproduce and distribute digital content on the internet. Owners of digital content have always had problems controlling and protecting their digital intellectual properties despite the copyright laws in place. With blockchain, creatives can now store their copyrights as smart contracts to reduce and even eliminate unauthorized redistribution risks. Apart from protecting intellectual property rights and combating counterfeit crime, it can provide access to investors by fractionalizing asset ownership.

Blockchain applications

The number of Blockchain jobs has soared enormously in the last two years. This is due to the promising applications of blockchain in many industries, which can increase efficiency, reduce cost and ensure credibility by using the technology. Of the major applications provided by blockchain, we’ve highlighted a few.

Smart contracts

Smart contracts can be seen as simple contracts that are executed when specific conditions are met. They are automated self-executing deals with specific instructions written on its code. This means that in a supply chain or a payment transaction, smart contracts can be built to ensure the requirements are met, from the provider’s product quality to the buyer’s available funds. One of the most well-known blockchain used to build smart contracts is Ethereum (ETH).

Sharing economy

By eliminating the middlemen, blockchain allows for P2P payments between providers and consumers. This direct interaction can be seen as a “sharing economy”, where traditional businesses such as Uber and Airbnb are seeing blockchain competitors jump in popularity.

Governance

From administrative tasks to data management, to voting, blockchain can be implemented in many ways in the governance sector. In Spain, the government of Catalonia invested in blockchain in its public administrative activities to expedite processes. In Japan, a city in the north of Tokyo has tested a polling system based on the blockchain, where the voters cast their votes only through a system that reads their national ID card number. This decreases the chances of fraud and malpractices in elections, turning the process more transparent and less subject to corruption.

Tokenization of assets

Lately, it seems that everything is being tokenized on Blockchain, from painting to real estate. Tokenization is a method that converts rights to an asset into a digital token. Each token represents a share of the underlying asset. The token is issued on a platform supporting smart contracts. Most recently, an Andy Warhol multi-million dollar painting was tokenized through an auction entirely conducted using smart contracts.

AML and KYC

AML/KYC solutions based on the blockchain are increasing. These two practices are labour intensive, long and costly. By applying blockchain, the costs can be reduced while monitoring and analysis effectiveness increase exponentially. From analysing transactions to doing a background check, everything can be done and stored on the blockchain.

What to expect?

Bitcoin (and cryptocurrencies) are frequently mixed with the blockchain. While one is the backbone of the other, their applications are distinguished. Their impacts are being felt across different industries around the world. They are expected to change B2B transactions, governance, payment systems, humanitarian aid, among many others. We are most likely to start using blockchain without noticing, as its adoption is becoming mainstream. Meanwhile, cryptos continue to be regulated as the skepticism around is slowly fades away. The predictions, which were once negative, have become relatively positive, as this new revolution paves the way to a new way of doing.

Has blockchain technology or cryptocurrency been impactful in your life so far? If so, how?

An intriguing discussion is worth comment. I believe that you need to publish more about this subject matter, it may not be a taboo subject but usually folks don’t talk about these issues. To the next! Many thanks!!

We found your publish and pays to for all. With thanks

Looking forward to reading more. Great blog post.Really thank you! Will read on…

Very neat article.Really looking forward to read more. Keep writing.